Stop Optimizing for Conversion. Start Building for Commitment.

Why the best fintech products have mastered intent and trust-building and what every PLG team can steal from their playbook

👋 Hi, it’s Gaurav and Kunal, and welcome to the Insider Growth Group newsletter, our bi-weekly deep dive into the hidden playbooks behind tech’s fastest-growing companies.

Our mission is simple: We help you create a roadmap that boosts your key metrics, whether you're launching a product from scratch or scaling an existing one.

What We Stand For

Actionable Insights: Our content is a no-fluff, practical blueprint you can implement today, featuring real-world examples of what works—and what doesn’t.

Vetted Expertise: We rely on insights from seasoned professionals who truly understand what it takes to scale a business.

Community Learning: Join our network of builders, sharers, and doers to exchange experiences, compare growth tactics, and level up together.

Who should read this: This piece is for product managers, founders, and growth practitioners at fintech companies or any high-consideration product (healthcare, B2B procurement, insurance, marketplace lending) where users need to trust you before they’ll commit.

The Playbook Has Already Changed

Every PM is taught the same thing: reduce friction, increase conversion. It’s the foundation of PLG. Free trials, instant access, zero-click signups. The playbook works beautifully until your product is one where users need to trust you before they’ll commit.

Look at what’s actually winning in 2026. Hims and Noom run multi-minute intake quizzes before they’ll even show a price. Ethos Insurance walks users through a long underwriting flow and turns it into a confidence builder. Every neobank worth its valuation has a deep, narrative-driven onboarding sequence.

They’re growth-optimized products that have figured out something the classic PLG playbook missed:

Users have two needs: instant confidence in the decision (”is this right for me?”) and the outcome they came for. You can’t always deliver the outcome fast. But you can always deliver the confidence.

A well-built funnel delivers that instant gratification through narrative. It tells users who the product is for, what’s going to happen, and why each step exists. The friction is incidental. The intent and trust-building is the mechanism.

The best fintech teams didn’t discover this by choice. Regulatory requirements, fraud risk, and real-world system dependencies made instant-value delivery structurally impossible. So they learned to design the funnel instead of shorten it. The result is a set of mechanics that any product can apply when the stakes are high enough that users need to trust you before they commit.

The answer is not that these products ignore friction. They repurpose it. Instead of eliminating required steps, the best teams turn friction into trust, turn delays into progress, and turn constraints into commitment moments.

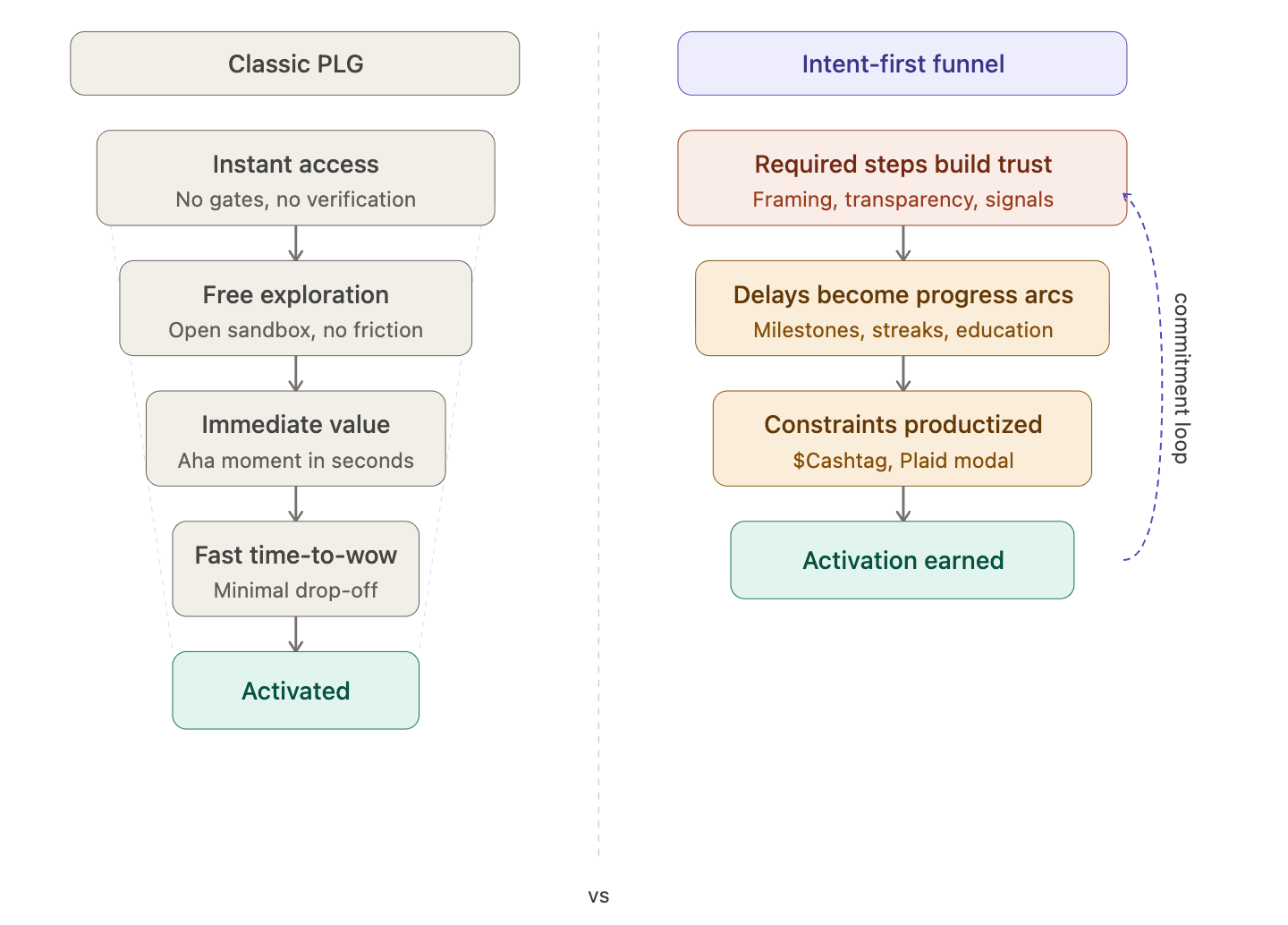

Classic PLG strips friction to reach activation fast. The best high-consideration products can’t so they design the friction to build intent and commitment instead.

Where Classic PLG Breaks

The Traditional PLG Playbook

In SaaS and consumer your job is to get a user to an “aha” moment as fast as possible. Reduce every click, every form field, every moment of cognitive load between signup and value delivery. This works because the underlying product is stateles - you can explore, fail, reset, and try again.

Why This Breaks in High-Stakes Products

Fintech operates under fundamentally different constraints that make instant-value delivery structurally impossible for most products:

Regulatory requirements (KYC, AML, BSA)- you legally cannot open an account without verifying identity

Fraud risk and liability- real money is moving; abuse has immediate financial consequences

Real-world system dependencies- banks, credit bureaus, and card networks don’t have instant APIs

Physical dependencies - issuing a card, moving money, or pulling credit data takes time by design

What happens is that traditional PLG metrics underperform. Onboarding takes longer, time-to-value is delayed, and drop-off during regulated steps is high. The mistake most fintech PMs make is treating these as optimization problems—trying to shorten SSN entry, hide funding steps, or rush credit decisions. The winning move is to treat these constraints as intent and trust-building opportunities.

Three Ways Industry Leaders Build Intent and Trust

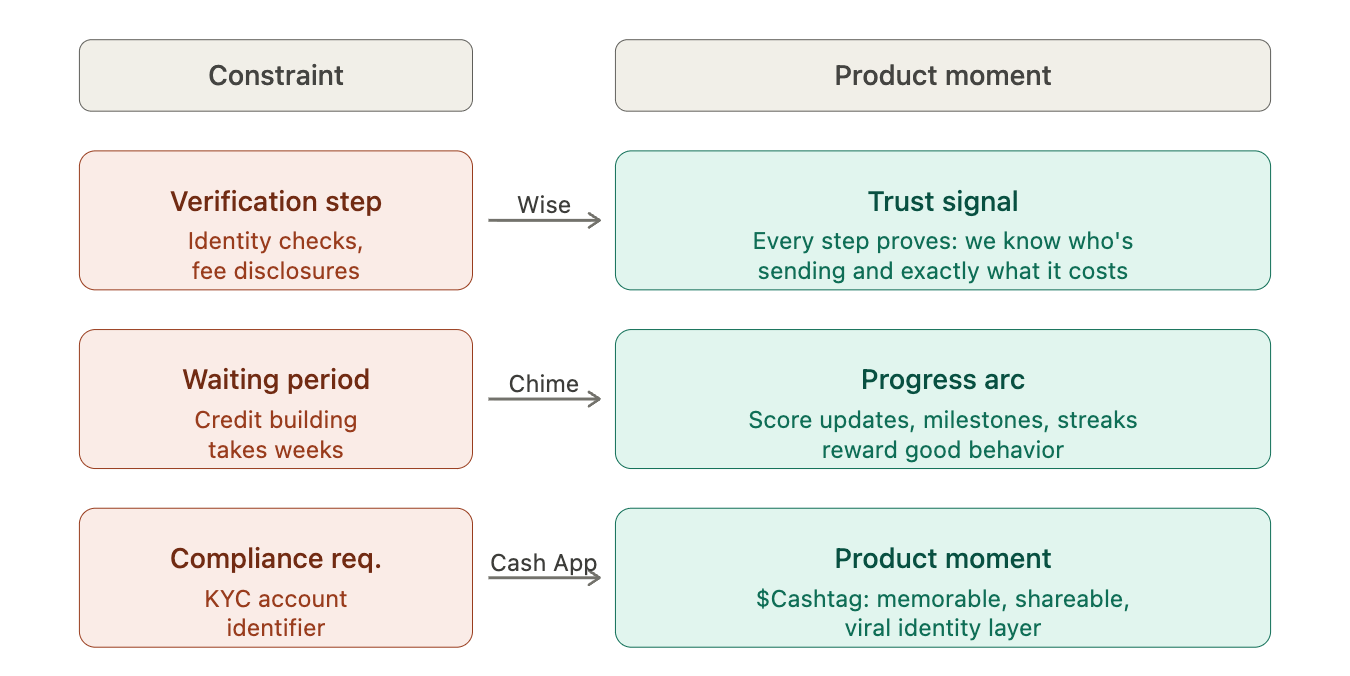

1. Required Steps as Trust Signals

In most products, a verification step is an interruption. In high-stakes products, it’s a signal proof that the product takes the user’s situation seriously.

Wise transforms international transfers into a multi-step verification experience: identity checks, compliance prompts, a transparent breakdown of the exchange rate, and a line-by-line fee breakdown before you confirm. On paper, this is more steps, more reading, more work. In practice, users trust Wise more because of it. Every step communicates: “We know who’s sending, we know who’s receiving, here’s exactly what it costs.”

Stripe does the same for businesses. Onboarding requires tax IDs, beneficial ownership details, and bank verification. The payoff is twofold: it increases perceived legitimacy for the merchant, and it protects Stripe from the fraud that would otherwise price out smaller players. The required step earns both sides of the market.

2. Unavoidable Delays as Progress Arcs

In high-consideration products, the “aha” moment is often days or weeks away. Credit scores don’t update overnight. Cards take 7–10 days to arrive. Loan approvals depend on bureau pulls. The temptation is to distract users during the wait. The better move is to make the wait itself meaningful—to give users instant gratification on the decision even when the outcome takes time.

Chime’s SpotMe and Credit Builder are built around this principle. You don’t get a credit line on day one. You open an account, fund a secured card, spend, and pay it off—and Chime reports each action to the credit bureaus. The delay is reframed as a reward for good financial behavior. Progress bars, credit score updates, and milestone notifications turn a multi-week process into an engagement loop.

Robinhood’s waitlist strategy for new product launches is a masterclass in turning operational delays into growth assets. Banking partnerships for products like Robinhood Retirement require hard evidence of demand before a bank will commit. Robinhood used waitlists to generate that evidence and added viral mechanics (invite a friend to move up the list) that converted the delay into a referral engine. The wait became both negotiating leverage with financial institutions and a live signal of organic demand.

3. Constraints as Commitment Moments

Compliance and fraud controls feel like guardrails imposed by the legal team. To the best fintech PMs, they are a design surface and sometimes the best one you have.

Cash App and Venmo took a mandatory KYC requirement - assigning account identifiers and turned it into a product feature. Rather than displaying an account number, they asked users to pick a $Cashtag or Venmo handle: memorable, customizable, shareable. The KYC flow still runs underneath, but the user-facing moment is “pick your identity,” not “here is your account number.”

Cash App extended this further with the Cash Card, a customizable physical debit card with drawings and emojis - turning the slow process of card issuance into something users looked forward to.

Plaid took the single most dreaded moment in consumer fintech—linking a bank account—and rebuilt it as a clean, branded, trusted flow that users now recognize across hundreds of apps. The friction did not go away; it got productized into a commitment signal. Seeing the Plaid modal now communicates: “this app handles your bank credentials the right way.”

Three companies, three constraints and three teams that chose to design them instead of bury them.

Introducing Reuben George

Reuben George was a Senior Director of Product at Self Financial, where he led Growth, Marketplace, and AI Advisor. Before Self, he was Principal PM at HubSpot and a product lead at Square and Intuit building his career at the intersection of fintech and PLG. He's currently building his own startup.

What is Self Financial?

Self Financial is a consumer fintech company focused on credit building. It’s designed for people with thin or damaged credit histories who need a low-risk way to build a track record. Its product ecosystem includes:

Credit-builder loan — the flagship product. Borrowers don’t receive the money upfront; payments are held in a savings account and released at the end of the loan term, while each on-time payment gets reported to all three credit bureaus.

Secured and Unsecured credit cards — lets users graduate from the loan into a revolving credit product, using their accumulated savings as collateral with no separate deposit required. From that, they graduate to unsecured credit cards with no collateral.

Early Wage Access — gives users the ability to draw against earned wages before payday, with underwriting that assesses income and spending patterns to determine eligibility and limits.

Bill Reporting — takes recurring payments users are already making (rent, utilities, phone bills) and reports them to the credit bureaus, turning everyday expenses into credit-building moments without requiring any new financial product.

Each product serves a different job for the same core user. But as the product line grew, so did the complexity of getting each user to the right starting point.

The two case studies below come from inside that transition and illustrate both what the team got right and what had to be rebuilt from scratch.

Case Study 1: Turning Onboarding Required Steps from a Drop-off Wall into a Trust Moment

Context

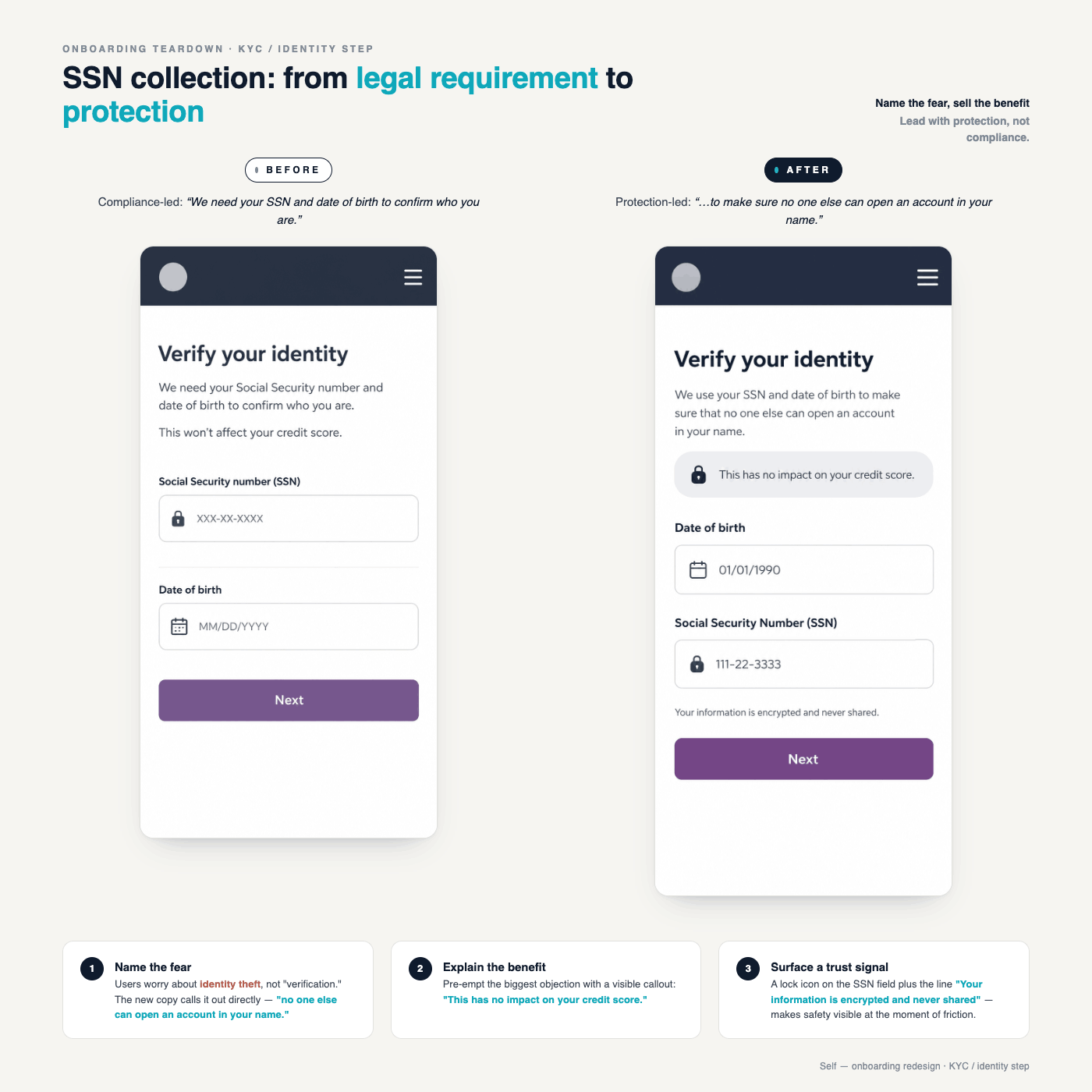

KYC (Know Your Customer) is a federal regulatory requirement for financial accounts. As part of KYC and to reduce fraud, most consumer fintech products need Social Security Number, Home Address, Citizenship status, Phone Number, among other pieces of information. However, these are also consistently the highest drop-off points in the onboarding flow, across the board. Users are wary of sharing this information with a company they’ve just discovered. They’re worried about their identity being stolen, or receiving unsolicited contact, or being chased by debt collectors. These challenges were faced by Self’s customers too.

Problem

Originally, these high-dropout steps (like SSN, phone number, home address, etc.) were framed as regulatory requirements. Framing these as regulatory requirements helped explain to users why that information was asked, which helped improve drop-off rates marginally, since the users at least understood that it was a requirement and not a choice.

However, it still didn’t address users’ fears that this information could risk being used for unintended purposes.

The regulatory framing was product-centric (”we need this because of XYZ reasons”) rather than user-centric (”here’s why this helps you”). The step didn’t build intent or feel like a value exchange.

Solution

The team conducted user research to understand the underlying fears of users at this step, then ran a structured copy and UX experiment across multiple variants. All winning variants shared a common theme: they named the user’s fear, explained the benefit to them, and surfaced a visible trust signal.

The winning copy reframed the ask entirely. Instead of leading with the legal requirement, it led with protection. For example, for the SSN collection step, a protection-led framing would be:

“We use this to verify that you are who you say you are and to protect you from identity theft.”

The step also added a lock icon and a tooltip explaining that the data was encrypted and securely stored.

For the Phone number step, we went from a defensive framing (”We won’t spam you or share your information”) to an offensive framing in order to make users more confident. The updated framing was:

“We use this information to protect your account. You have explicit control over whether to receive marketing updates and offers.”

The change was more subtle than the SSN step, but we did a few things for this step:

We primed our marketing outreach in a positive light (”Marketing updates”, rather than “Spam”)

We introduced calming imagery

We used the entered phone number as a form of 2FA authentication, giving users additional account security

Impact

Significant lift in conversion through the SSN step, carried over to a significant increase in the number of KYC users per week and accounts opened

Key Learnings

Regulatory requirements are not fixed conversion ceilings. They’re design problems. The step did not change; the framing did.

Name the user’s fear before asking for the data. Acknowledging the concern removes it as an obstacle.

If you’ve gotten this far, you may be ready to navigate to the 🔥 section and check out our Playbook now.

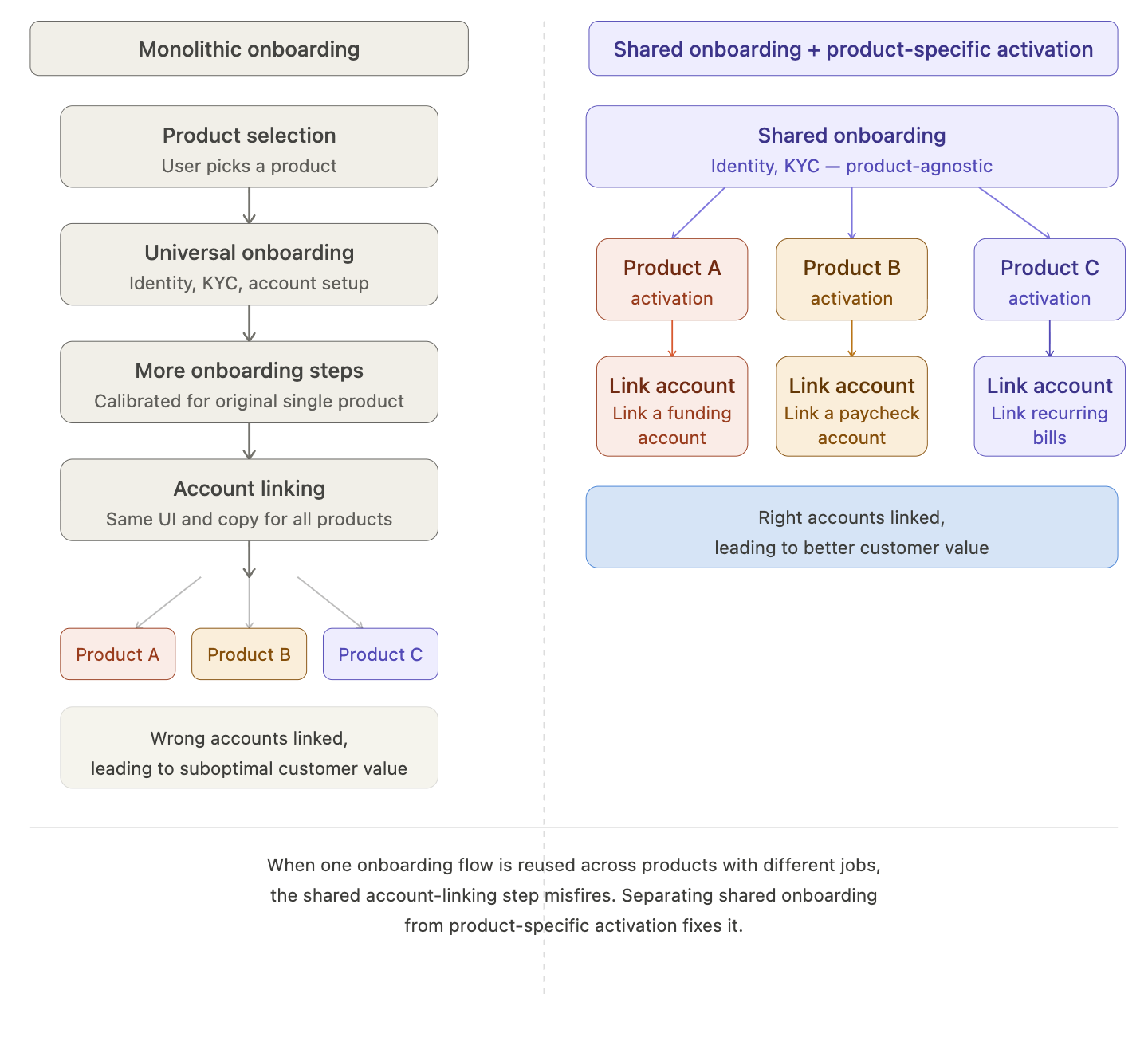

Case Study 2: Rebuilding Account Linking for a Multi-Product Ecosystem

Context

As a fintech company grows from a single product into a multi-product ecosystem, its original onboarding flow gets reused for each new product. It’s faster to ship. But it creates a hidden problem that only becomes visible at scale.

Account linking (typically done via Plaid, with a manual bank entry fallback) is a required step across most consumer fintech products. On the surface, it looks like the same step every time: ‘Connect your bank account.’ In practice, it serves a completely different purpose for each product—and a flow built for one product can silently misfire for all the others.

Problem

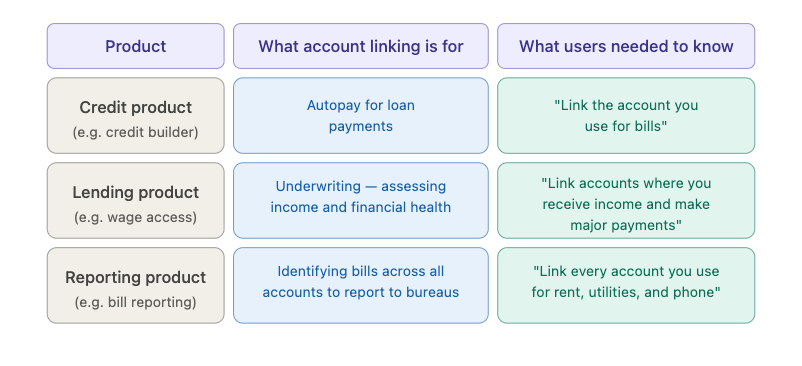

Three products. Three different jobs for the same UI:

The problem isn’t the account-linking step itself — it’s that the same generic UI was doing three completely different jobs without telling users what any of them were.

For a lending product, account linking is an underwriting input. The product needs to see the accounts where a user receives their paycheck and makes their biggest recurring payments — rent, car, utilities. Without that picture, the eligibility model is working with incomplete data, which means users get rejected or approved for less than they actually qualify for. Not because they’re a bad candidate, but because they linked their secondary savings account instead of their primary checking account.

For a reporting product, account linking is a data coverage problem. The product can only report payments it can see. If a user pays rent from one account and utilities from another but only links one of them, the product misses half the transactions that could improve their credit score. The user does everything right and still gets a fraction of the value.

In both cases, the user had no idea. The UI just said “connect your bank account.” So they connected the first one that came to mind and the product quietly failed them.

Solution

The fix required a first-principles redesign of what account linking meant across the product ecosystem. First, the team separated user onboarding from product activation:

Onboarding became the lightweight path to becoming a Self member: identity verification, basic account setup—steps every user needed regardless of product.

Product activation became product-specific. Each product owned its own flow, including its own framing of the account linking step.

The Lending product now explains: “Link the accounts where you receive your income and make your biggest payments. The more complete your picture, the more we can offer.”

The Reporting product now explains: “To report the most payments to the credit bureaus, connect every account you use for rent, utilities, and phone.”

The Credit product keeps its original single-account autopay framing.

Impact

Significant lift in page throughput at the account linking step across all three products

Significant lift in early wage access approval rates—underwriting received more complete financial pictures, leading to more accurate and favorable decisions

Significant lift in activation for bill reporting—more bureau-reported transactions led to more trade lines and improved users’ credit scores faster

Key Learnings

Onboarding debt compounds. A flow built for one product silently fails every product you add afterward. Audit your universal steps regularly.

“Why” is as important as “what.” Users who understand why they’re being asked to link a specific account link the right one. Users who don’t guess—and usually guess wrong.

Separating onboarding from activation is an architectural decision, not just a UX one. It affects how you build, how you measure, and how you scale.

What Replaces Classic PLG

Fintech doesn’t abandon the goal of PLG; it replaces the mechanisms.

The through-line across all four: when stakes are high, users optimize for safety and predictability, not speed. A product that communicates “here’s exactly what will happen, here’s where you are, here’s what comes next” consistently outperforms one that tries to compress time at the expense of clarity.

🔥 IGG Playbook: The Intent and Trust-Building Framework

You don’t need to work in fintech to use this framework. Any product with high-consideration steps - healthcare onboarding, B2B procurement, regulated marketplaces, expensive consumer purchases can apply the same three moves.

Step 1: Audit Every Required Step for Intent-Building Potential

Go through every required step in your onboarding or activation flow. For each one, ask: if this step was surfaced and explained well, would it make a user more confident and committed or less?

Steps that communicate “we’re protecting you” or “here’s what this does for you” should be moved forward and designed explicitly as trust moments, not hidden or minimized.

Steps that are purely administrative should be batched, minimized, and moved late.

Ask for each step: does the user understand why we need this, what we’ll do with it, and what we won’t do with it? If not, that’s your copy problem.

The SSN example says it all: the step didn’t change. The framing did. That’s the entire playbook in one sentence.

Step 2: Turn Every Unavoidable Delay into a Progress Arc

Anywhere a user has to wait - for a review, an approval, a data sync, a card to arrive - ask whether the wait could become a moment of intent reinforcement or engagement.

Add progress indicators. “Step 2 of 4” is always better than a spinner.

Turn idle time into education. What does the user need to know before your product delivers value? Teach it now.

Use milestones and streaks. Chime’s credit-building flow turns each payment into a proof point. What’s the equivalent in your product?

If there’s a business reason for the delay (partner onboarding, compliance review), tell users. Unexplained delays read as broken products.

Step 3: Productize Your Constraints into Commitment Moments

The step your legal or ops team considers a necessary evil is often the best candidate for a signature product moment.

Ask: can this mandatory step become a user choice? Cash App turned account identifiers into $Cashtags.

Ask: can this step be made visual or tactile? The Cash Card turned a 10-day wait into something users customized and looked forward to.

Ask: can this step build brand recognition? Plaid turned the most dreaded step in fintech into a trusted signal across the entire industry.

The constraints you can’t remove become brand assets if you design them intentionally.

The key distinction the best product teams internalize:

Conversion is not the same as commitment.

Stripping out steps gets more users in the door. Designing the right steps gets the right users to stay, fund, transact, and come back.

The PMs who understand that don’t spend their time removing friction. They build the narrative that earns it.

Want help on any product growth challenges you have?

Let’s talk